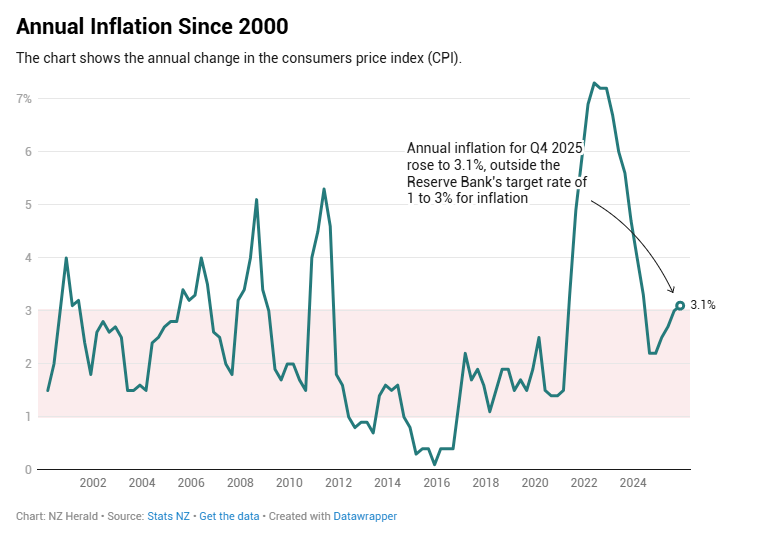

- Inflation concerns have surfaced with a rise to 3.1% at the end of 2025, slightly above the Reserve Bank’s 1-3% target. Despite this increase, the economy still has spare capacity, so inflation is expected to ease again, possibly delaying interest rate hikes until later in 2026 rather than early 2027.

- First-home buyers continue to lead the property market, reaching 28.4% share in the last quarter of 2025, the highest in recent years. Favorable conditions such as lower mortgage rates, more listings, and KiwiSaver support contribute to this trend. Many first-home buyers enter the market with low deposits, helped by bank lending allowances, and some may save on housing costs compared to renting.

- After a long period of declining activity, the services sector showed growth in December 2025, signaling some economic strengthening beyond property markets.

- Migration patterns may be shifting positively, with net migration increasing slightly after a low point. This could improve rental demand, which landlords have been watching closely amid recent rent weaknesses.

- Mortgage activity data to be released soon will provide insight into whether bank cashback offers have triggered more switching between banks and if recent easing of loan-to-value ratio (LVR) rules has changed lending behavior. Initial reports suggest strong bank switching but only tentative movement regarding LVR relaxation.

Overall, the housing market faces mixed signals with inflation causing some caution but strong demand from first-home buyers supporting market activity, while economic and migration trends suggest potential for steady recovery and rental market improvement

Source from Oneroof: by Kelvin Davidson

Additional commentary from him can be found at https://www.oneroof.co.nz/news/finance/inflation-blow-raises-spectre-of-early-interest-rate-rise-but-how-soon-48849

The opinions and research contained in this article are provided for information purposes only, are intended to be general in nature, and do not take into account your financial situation or goals.