As 2026 unfolds, understanding interest rate trends is crucial for property managers and home buyers planning their next financial steps. According to Trade Me Property’s latest analysis, the outlook from major New Zealand banks suggests rates will mostly plateau or rise modestly during the year.

- Bank Predictions:

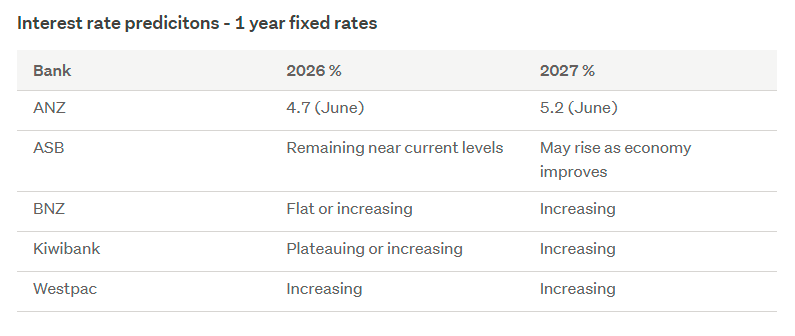

Major banks like ANZ, Westpac, ASB, BNZ, and Kiwibank expect one-year fixed mortgage rates to either remain near current levels or gradually increase through 2026. ANZ forecasts the rate at about 4.7% midyear, with a slight rise in 2027. Some lenders see potential rate increases as the economy strengthens .

- Official Cash Rate (OCR) Outlook:

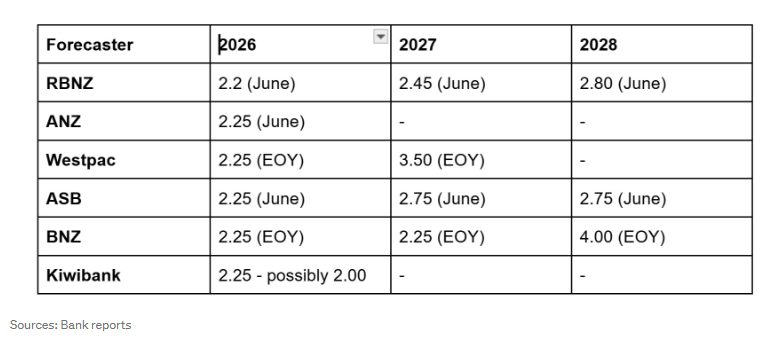

The Reserve Bank’s official cash rate, which heavily influences retail lending rates, is widely expected to maintain a steady or gently rising trend during 2026, providing a foundation for mortgage rate projections .

- Expert Advice on Fixing Mortgage Rates:

Mortgage experts offer varied views on how long borrowers should fix their rates. Some recommend one-year fixes as a flexible option, while others suggest splitting terms or opting for longer fixes depending on personal circumstances and market views. Carefully weighing break-even points is advised before committing .

- The Reserve Bank’s Role:

The Reserve Bank remains a key player, adjusting policy rates to balance inflation and economic growth. Its decisions will continue shaping the direction of mortgage interest rates throughout 2026 .

- Key Takeaway:

Given the nuances and uncertainties in economic forecasts, seeking expert financial advice tailored to individual situations is important before making mortgage decisions. Staying informed about market movements helps property managers guide clients and plan investments wisely .

This summary aims to equip property professionals and home buyers with up-to-date insights to navigate the evolving interest rate landscape confidently in 2026.

Source from trademe: https://www.trademe.co.nz/c/property/article/Interest-rate-predictions

The opinions and research contained in this article are provided for information purposes only, are intended to be general in nature, and do not take into account your financial situation or goals.