Five Things You Need to Know About the Housing Market

- Inflation Headlines Return

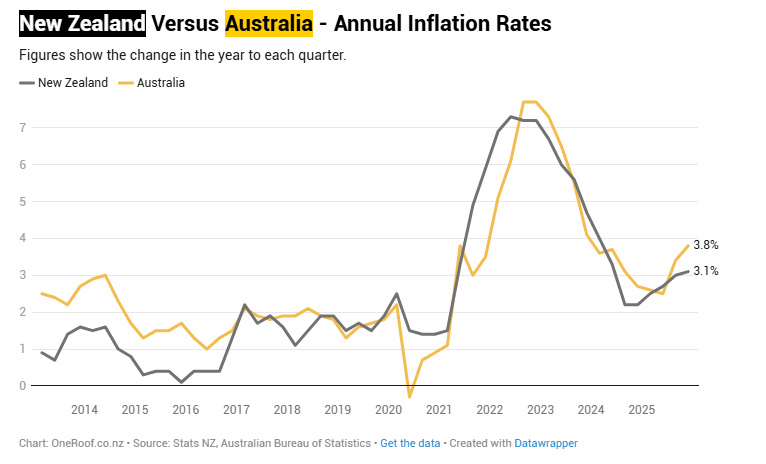

The Consumer Price Index (CPI) for Q1 2026 will be released on Tuesday. After Q4 2025’s 3.1% inflation (slightly above the target), fuel price increases in March may push inflation higher again. Although the Reserve Bank plans to “look through” initial fuel cost effects, inflation could rise above 4% in Q2, with concerns about broader price pressure, wage demands, and inflation expectations.

- Economic Slowdown Accelerates

March’s NZ Activity Index is expected to show further slowing, reflecting drops in business and consumer confidence and weaker manufacturing and services activities. This slowdown complicates the Reserve Bank’s balancing act between inflation and GDP risks.

- Housing Sales Remain Soft

About 8,900 properties sold in March, down 2% compared to March 2025, marking the third consecutive monthly decrease. Despite the modest drop, high inventory and buyer pricing power persist. Given delayed impacts on confidence, mortgage rates, and buying decisions, sales may continue to soften in coming months.

- First-Home Buyers Strong, Investors Mixed, Movers Cautious

First-home buyers made up 27.5% of purchases in early 2026, near record highs, benefiting from stable prices, temporarily lower mortgage rates, and lower deposit barriers. Mortgage-holding investors continue buying but face challenges like weak rents and rising costs, leading some to reduce portfolios. Owner-occupiers moving homes remain subdued amid economic uncertainty and global tensions

- Migration Could Rise Further

February saw the strongest net migration in two years, with nearly 25,200 annually, driven by increased arrivals and fewer departures. This trend is favorable for tenant demand, though March and beyond may show variability. New migrants seeking safety and residents staying put might boost the housing market.

Source from Onerrof: by Kelvin Davidson.

Additional commentary from him can be found at https://www.oneroof.co.nz/news/market-on-a-knife-edge-what-falling-sales-and-a-jump-in-inflation-could-mean-49321

The opinions and research contained in this article are provided for information purposes only, are intended to be general in nature, and do not take into account your financial situation or goals.